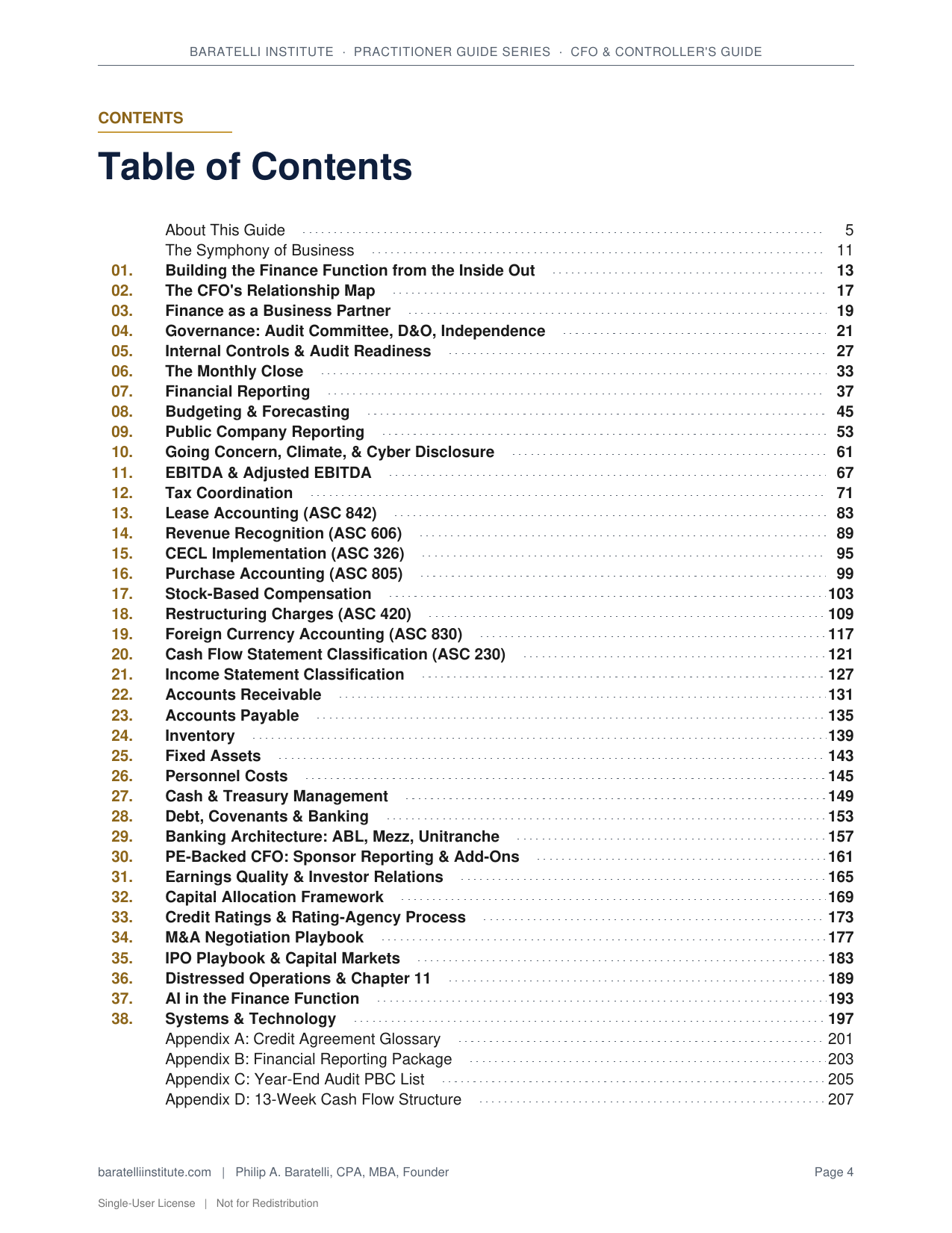

38 chapters across 5 parts plus appendices including the AI Tool Prompts library (50+), comprehensive glossary, and index. Page counts approximate.

PART I · The First 90 Days & Foundations

1What CFOs Actually Dop1

2CFO Persona Routing & How to Read This Bookp7

3The CFO's First 90 Daysp13

4Building the Finance Function from Scratchp25

5Close Calendars & Reporting Cadencep35

6Books, Records & the Audit Trailp43

PART II · Technical Accounting & Modeling

7Three-Statement Modeling at PE Depthp51

8Revenue Recognition & ASC 606p65

9Lease Accounting & ASC 842p73

10Stock Comp & ASC 718p81

11Working Capital Managementp89

12Cash Flow Forecasting (13-Week + LRP)p99

13Tax Provision & Deferred Tax Mechanicsp107

PART III · Capital, Debt, Treasury

14Capital Allocation & CapEx Disciplinep115

15Tech Stack & ERP Selectionp125

16AI in the Finance Functionp135

17Cyber, Data Security & SOC 1/2p147

18Audit Prep, SOX, & External Auditor Managementp155

19Pricing Strategy & the CFO's Rolep165

20Customer Profitability & Cohort Economicsp173

21Sales Operations & the CFO-CRO Partnershipp181

22Debt Covenants & Lender Managementp189

PART IV · Operating & Performance

23PE Operating Partner Cadence (if PE-backed)p199

24Inventory Operations & the Inventory CFOp209

25Manufacturing CFO Specificsp221

26Services / Software CFO Specificsp229

27Multi-Entity / Multi-Currency Operationsp237

28KPI Dashboards & the Monthly Packp247

29FP&A Cadence & Forecast Disciplinep259

30Treasury & Bankingp267

31Insurance, Risk & Captive Programsp277

32Estate Tax, §1202 & Liquidity-Event Planning (for the founder you serve)p287

PART V · The People & the Career

33Hiring & Comp Structurep297

34Building & Managing the Finance Teamp307

35Board Management & the Audit Committeep315

36The CFO-CEO Partnershipp325

37Common Mistakes & the Recovery Playbookp333

38CFO Career Architecture (private, public, fractional, founder)p341

Appendices

ASample Monthly Reporting Packp349

BSample 13-Week Cash Flow Forecastp353

CSample Operating LRP (5-year)p357

DVendor Scorecard / Cyber Scorecard / AI Readiness Scorecardp361

NAI Tool Prompts Library (120+ practitioner-grade prompts)p369

GComprehensive Glossaryp381

IIndex of terms with page referencesp389